Three years ago, i planned to raise an investment in my company. The first question i asked myself then was, How much equity the investor will take for the money he will invest. That was a very hard question …

The first thing came to my mind then is to go for a financial expert to do the company valuation. Their rates was shocking and i get back and decided to do it myself. From the first moment i decided that, i realized that it will take a lot of time, could be months. I am an engineer, but i already have a good accounting background from a 3 months dedicated course. And hence I started by Google and red a lot of articles about “company’s valuation” just to decide the study road map. After a one month of reading articles. i searched for a course about financing. Coursera was a very good destination and i got a course there for 8 weeks from Michigan university. After that course, i went back and red again all the articles i red before. and you can definitely say that this article is a summary of my findings. I hope you like it and find it useful, if you do please share it and leave me your feedback and comments.

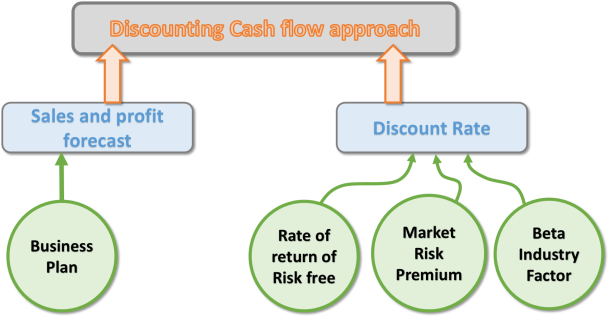

For a company that all its value is in intangible asset like a brand or software or portal, You will not probably find a way to valuate it except with the “discounting cash flow” approach. In this approach, you valuate your company with the business it can generate in the future. simply, how much business you can do in the future defines your current value.

to work with this approach you need to know two major things:

- Your Sales and profit forecast over five years at least.

- The discounting Rate (the rate you going to use to discount your future cash flow into present value).

In a recent article i have wrote about “how to build a financial cash flow plan“. and Soon i will write about “how to build your business plan“. This article is focusing on how to calculate Discount rate.

A major factor in applying discounted cash flow approach is the discount rate. Discount Rate is calculated based on three sub factors, below we will talk about how these three factors are calculated and how they are affected by the country you live in. I have made two examples, one from USA where i live and invest now, and the other from Egypt, where i used to do business before.

Rate of Return of the risk free:

The risk-free rate of return is the theoretical rate of return of an investment with zero risk. It is a theoretical concept as there is no risk free business. and it is used as starting point for calculating the cost of equity and capital. For instance, a bank considering a loan application will start with the risk-free rate and then add additional interest for other risk components such as default risk, inflation risk, and, if the loan is to a foreign company, currency risk.

Usually it is calculated based on the return on government bonds as it could be the most safe investments.

In Jan 2015

- Return on USA ponds is expected to reach 3.4% at the end of 2015 for 10 years bond.

- And it is almost 15.27% for Egyptian government over the same period.

Definitely we can not take the market risk free factor as a discount factor for our business. the Discount factor in other project rather than government bond is higher, because the risk is higher, so how much higher is it …

Market Risk premium:

Market Risk premium are percentages that you just pick it up from the internet, we don’t much care about how it has been calculated. It reflects the economical and political stability of the country.

As per Jan 2015:

Egypt: Moody’s rating: Caa1, country risk premium is 4.42%.

USA: Moody’s rating: Aaa, Country risk premium is 0.00%

In 2011

Egypt: Moody’s rating: Ba1, and the country risk premium is 3.6%

Ref: http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/ctryprem.html

Beta industry factor:

In finance, Beta is generally a measure of risk. so each industry has a calculated beta factor. it changes every year based on global economy health. You can check beta factor of each industry from this link:

http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/Betas.html

By jan 2015…

software (entertainment): 1.12

Software (internet): 1.19

Software (system and applications): 1.1

so based on three mentioned factors and considering that i work in the software (internet) industry then the discounting factor in Jan 2015 is as follow:

For USA: (3.4%+0.00%) * 1.19 = 4.046%.

whereas for Egypt: (15.27%+4.42%) * 1.19 = 23.43%

Now you know the Discounting factor in which you going to use to discount all your future cash flow that your company can make … into today value.

Now you must have cash flow forecast for 5 years ahead. please review my article ” How to Rock your start-up project Financial plan – Part.1 (Build the template)” and i prefer you plan your forecast based on this template.

Also review the article “How to Rock your start-up project Financial plan – Part.3. (Financial decision criterion’s)” to know how to calculate your project Net present value. when you calculate your Net present value, you will use the discounting factor we calculated before.

Many entrepreneurs stop here and assume that the NPV is equal to their startup value, actually i did that before… 🙂

I think you may do that, if your idea is not tested in the market yet, and you have no good prove that your idea can fulfill and meet your forecast expectations. But if your idea is already generating money and you used your cash flow history as a prove that you can fulfill and meet your forecast, then your will be less estimating your company value if you sold it at the NPV.

You have calculated your NPV based on a 5 years cash flow. In real life, your project will not stop and terminate at the end of the 5 years… right ? … your project will continue generate money, and the company could last for decades making profits. how do you include this factor.

Here comes a factor named: Perpetuity net cash flow (NCF). A perpetuity is a constant stream of identical cash flows with no end. we will keep things simple and make it equal to the net profit at the end of the fifth year. (assuming that you continue generate the same profit every year, not more nor less)

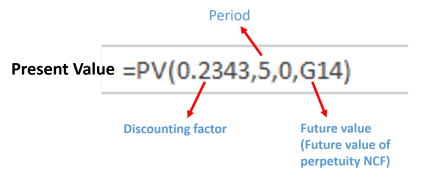

Then we will calculate the “Future value of perpetuity NCF” by dividing the perpetuity NCF over the discount rate calculated above.

Then we will calculate the Present value of the Future value of perpetuity NCF.

And finally the project value is equal to the NPV over the 5 years and the present value of the Future Value of perpetuity NCF.

Feeling lost 🙂 …. here is the Example…

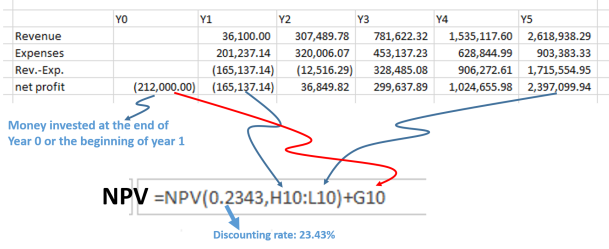

I will make an example using a cash flow stream of one of my projects. i will assume that the project will have the same cash flow stream in Egypt and USA and valuate the project based on the discounting rate calculated above.

In Case the project is valuated in Egypt:

NPV = 1,115,929.50$

Perpetuity net cash flow (NCF) = 2,397,099.94$ (net profit in the last year).

Future value of perpetuity NCF = Perpetuity net cash flow / Discount factor = 2,397,099.94/0.2343 = 10,230,900.30$

Present value of perpetuity NCF = 3,571,167.39$ (see the following figure to know this value is calculated)

Then the company value Equals 1,115,929.50 + 3,571,167.39$ = 4,687,096.89$

Now lets repeat it with the discount factor in USA.

NPV = 2,769,570.18$

Perpetuity net cash flow (NCF) = 2,397,099.94$ (net profit in the last year).

Future value of perpetuity NCF = Perpetuity net cash flow / Discount factor = 2,397,099.94/0.04046 = 59,246,167.56$

Present value of perpetuity NCF = 48,588,408.69$

Then the company value Equals 2,769,570.18 + 48,588,408,69$ = 51,358,050.87$

An important note i should mention here, is that i compared USA to Egypt, assuming that the project will make the same cash flow stream in both countries which is not right, and assuming the same taxation rate, which is not right too.

I just fixed these two conditions to have some insights on the effects of Risk free return and market risk premium.

I did my best to simplify it, if you have a basic knowledge about financing, i mean you know about the NPV, FV, …etc. then mostly you will not find a problem understanding this article. If not, you may need to read about it from the internet. and you may follow the steps i provided to you in this article even if you don’t fully understand it.

Finally, if you like it please share it. If you have any question, i will be very happy to answer you…

You can also download the template from Here

40.387989

-74.335286